How to Check Your Credit Score in the Philippines

Key takeaways:

- If you are planning to borrow money for housing loan or a car loan, it is important that you take care of your credit score

- If you have a bad rating, you will not be able to borrow money, especially large loans from banks

- Small loans up to ₱25,000 can be approved even with a bad credit history

Table of Contents

A credit score is a measurement of your “credibility” as a borrower. The higher your score, the more likely you will get approved for a loan or credit card. You can achieve and maintain your good credit standing by paying bills on time and only applying for loans that you need.

In the Philippines, only a few people know about their credit information or credit standing. Verification is done through the Philippine credit scoring system. Let’s find out how to know your credit score in the Philippines and why this is important.

- Only 1 Valid ID needed to apply

- Get your first loan with 0% interest

- Get up to ₱25,000 in just 4 minutes

What is Credit Score?

There are several terms that people may find confusing. Below, we will define the differences between good credit score, report, and history.

A credit score is a three-digit figure which determines your creditworthiness. There is no single global standard as to how the ratings are made. Some institutions use letters, while some use numbers. No matter what they use, your goal is to have a high rating.

A high credit score means that you are trustworthy in the eyes of banks and creditors, and that you are a good borrower who pays your debts.

On the other hand, if your credit standing is low, it means that you have a history of not paying your loans or bills on time. If a lender sees this, he is not going to approve your loan or credit card.

There are many factors that affect your credit information in the Philippines, such as:

- Age

- Annual income

- Existing Debt

- Borrowing history

- Timeliness of payments

- Employment Status and History

- Number of Inquiries on Credit Report

- Type and Number of Credit Accounts

- Relationship with Financial Institutions

Not all financial institutions use the same factors, and not all of them use the same formula. What matters here is that you can get a good credit rating in the Philippines by paying your debt on time.

Key Factors Affect Your Credit Score

These factors affect your credit standing, so you should take note of these:

| Factor | Description |

|---|---|

| Payment history | Banks and private lenders will take a hard look at your credit payment history – how often do you pay, how much you’re paying, and if you’re paying on time. |

| Types of credit use(d) | This pertains to the variety of credit you’ve utilized, such as personal loans, credit cards, housing loans, and car loans, if applicable. |

| Length of credit history | This refers to the duration for which you’ve held your credit cards or loans. A longer credit history generally reflects positively on your creditworthiness. |

| Amount of credit owed | This indicates the total owed amount, encompassing both loan balances and credit card debts. Higher debt levels might hinder approval for new loans or credit. |

| New credit applications | Your credit report will take note if you have pending applications for new credit, and how often you are applying for new loans. Having new credit all at once is not a good look. |

👉 Also Read How to Get

a Student Gadget Loan in the Philippines

What is Credit Report?

A Credit Report in the Philippines [1] is a document which contains your credit score. It also includes details about you, plus your credit history if the financial institution needs it.

Here are some of the details you will find in a credit report:

- Your name, address, gender, age, address;

- Details of your credit line as if you have a credit card

- Details about your public records such as if you filed for a bankruptcy

- List of institutions that have asked for your credit report in the past

Different credit reporting bureaus have different data reporting methods. Not all of them have the same access to your personal and public financial history, so this information is going to vary.

What is Credit History?

Your credit history refers to your credit activity, the credit cards and loans that you have and whether you’re paying them on time. As the term implies, it refers to your historical behavior of using credit and paying loans in the past.

Did you pay on time and in full or did you bailout?

The credit history is part of the report. If you borrowed, for example, ₱100,000 five years ago and paid only ₱50,000, this history will be included in your financial credit history. Once a lender sees this, the natural tendency is for the lender to say that you are a high-risk individual.

Some credit history reports also show your bank accounts, average daily balance, spending habits with your credit card, and many more. The credit history is used to determine your final credit score in the Philippines, and it also tells a lender whether you are worthy of another credit or not.

How to Check My Credit Score in the Philippines

In the Philippines, individuals can obtain their credit report along with their credit score through the Credit Information Corporation (CIC) and its accredited credit bureaus. Here’s a summary of the process and other relevant details:

Credit Information Corporation (CIC)

The Credit Information Corporation (CIC) is the official public credit registry in the Philippines. It collects and maintains credit information submitted by financial institutions such as banks, lending companies, and other credit providers. Here’s how you can check your credit score through the CIC:

- Step 1: Visit the official CIC website (https://www.creditinfo.gov.ph) and navigate to the ‘Services’ section.

- Step 2: Register for an account if you are a first-time user, or log in if you already have an account.

- Step 3: Follow the instructions to request your credit report, which will include your credit score. The CIC partners with accredited credit bureaus, and you may be redirected to one of them.

- Step 4: You may need to pay a small fee to access your credit score and report. Prices vary depending on the credit bureau.

Note: The CIC does not directly calculate your credit score; it works with accredited private credit bureaus such as CIBI Information, TransUnion, and CRIF Philippines. They use the information from the CIC database to generate your score.

CIBI Information Inc. App

How to Check Your Credit Score in the Philippines online with CIBIApp? One of CIC’s accredited credit bureaus, CIBI Information Inc., has launched the CIBIApp. Through this app, you can obtain a copy of your credit report and credit score online.

- Access the app via your web browser at [cibiapp.cibi.com.ph] [3](https://cibiapp.cibi.com.ph/#/login).

- Character Verification: This process is done online through MeetMe, a video call feature of the CIBIApp. On the day of your online interview appointment, prepare the IDs you uploaded during registration.

- Receiving the Report: Your CIC Credit Report will be sent to the email you provided during your appointment scheduling.

Cost: Is a free credit report in the Philippines? A CIC Credit Report with a credit score from CIBI costs PHP 235.00 (VAT inclusive).

Disputing Errors:

- If you find any erroneous data on your CIC Credit Report, you can file a dispute online through the

- CIC’s [Online Dispute Resolution Process (ODRP)](https://www.creditinfo.gov.ph/online-dispute-resolution-process-0)[4].

- Filing a dispute is free of charge.

Note: The credit score is a service provided by CIC’s accredited credit bureaus and is derived from CIC’s credit reports. If you haven’t had any loan transactions in your credit report for the last two years, a credit score cannot be generated for you.

TransUnion Philippines

Another company where you can get your credit scores is called TransUnion. It is a global entity, and it is also the first credit bureau of the Philippines. Just go to the website and get your report in the Philippines.

There are 2 types of data here. The first one is a business reporting, which is for insurance companies, banks and lenders. If you want to know your credit scores and history in Philippines, you have to select a personal report. Loan companies check borrowers using credit scoring.

TransUnion is one of the leading credit bureaus in the Philippines and offers easy access to your credit score.

- Visit the TransUnion website (https://www.transunion.ph).

- Create an account or log in if you already have one.

- Request your credit score, which may involve a fee. TransUnion sometimes offers promotions that allow users to check their credit score for free.

Some banks and digital lending platforms offer free credit score checks for their customers. These are convenient ways to monitor your credit score, especially if you regularly use these banking platforms. For example, if you have an account with UnionBank, you can access your credit score through their mobile banking app. CIMB also allows its users to check their credit score for free via its app.

How to Check My Credit Score Ph for Free?

To check your credit score for free in the Philippines, there are a few options you can explore. While not all services offer completely free access, some do provide periodic promotions or free credit score checks for their customers. Here are the main ways you can check your credit score for free:

1. Banks

UnionBank offers free access to your credit score through its mobile banking app. If you are a UnionBank account holder, you can check your credit score without any additional charges.

- Download and log in to the UnionBank mobile app.

- Navigate to the section offering credit score monitoring (usually under “More” or “Credit”).

- View your credit score for free, as part of the bank’s value-added services for account holders.

CIMB Bank also provides free access to credit scores through its mobile app for users who have an account.

2. GCash

GCash, a popular mobile wallet in the Philippines, occasionally partners with credit bureaus to offer free credit score checks to its users.

- Open the GCash app and navigate to “Financial Services” or “GScore.”

- The app might provide your credit score, or a similar GScore, which reflects your creditworthiness.

Note: This is not always a full credit score from the CIC, but GCash often uses TransUnion data, so it’s a good reflection of your credit health.

3. Promotions from Credit Bureaus

Credit bureaus such as TransUnion and CIBI Information, Inc. may offer occasional promotions that allow you to check your credit score for free. Keep an eye on their websites or social media channels for these offers.

How to Get My Credit Report in the Philippines

Now, let us talk about how to get your credit report in the Philippines. A credit report provides a detailed record of your borrowing history, including your loan accounts, repayment behavior, and any defaults. So, how can you request your credit report in the Philippines?

✅ Credit Information Corporation (CIC): [2]. The CIC is the main source of credit reports in the Philippines, collecting data from various financial institutions. To get your CIC credit report, go to the CIC website and register for an account. They will guide you how to check credit history in the Philippines.

Note: The CIC credit report does not include a credit score, but it contains your full credit history, which is vital for lenders to assess your creditworthiness. Here’s how you can get your credit report from CIC:

- Visit the CIC website and follow the process outlined in the “Check My Credit Score” section above.

- Once you log in, request a copy of your credit report. The report will include a detailed breakdown of your credit history.

- Choose your preferred accredited credit bureau (TransUnion, CIBI, or CRIF) to generate the report.

You must complete the verification process, also known as Know Your Customer, and then proceed with the online application. The thing is that you have to personally visit the physical office of CIC in Makati City to be able to get your credit data if you do not qualify for the online reporting.

✅ TransUnion: Another company where you can get your credit report from TransUnion. It is a global entity, and it is also the first credit bureau of the Philippines. If you want to get an idea on your credit behavior, you can go to the TransUnion website and request for a report.

- Visit the TransUnion website and sign up for an account.

- Request your credit report, which will include your credit history with details of loans, repayments, and any defaults.

- Pay the applicable fee to obtain your report.

TransUnion gives out two types of credit score reports. The first one is business reporting, which is for insurance companies, banks and lenders. On the other hand, a personal report will show you your personal credit score and history here in the Philippines.

✅ CIBI Information, Inc. Credit Report: Another option is to get your credit report from CIBI.

- Visit the CIBI website and create an account.

- Request your credit report, which will include a complete record of your borrowing history.

- Pay the required fee for access to the report.

✅ CRIF Philippines: CRIF is another credit bureau that provides credit reports in the Philippines. You can access their services online:

- Visit the CRIF Philippines website (https://www.crif.com.ph/).

- Sign up for an account and request a copy of your credit report.

- Similar to other bureaus, a fee may apply for obtaining your credit report.

👉 Do you know How to Get

a Fast Cash without a Bank Account

Why are Credit Scores Important in the Philippines

You need to have a good credit rating in order to have a better standing and relationship with banks and financing institutions.

Having a good credit score gives lenders the confidence to lend money to you or give you new credit. It means that you are a good payer who does not miss a payment cycle. Having a positive credit standing allows you to have higher loan amounts at more favorable rates. Your bank may opt to waive your annual fees if you’re paying on time, too.

A good credit score also signifies financial stability. It means that you are responsible enough to have a stable income and not rely on loans for your daily expenses. Applying for new loans or credit cards every now and then is not a great look.

Your credit history will also affect your chances of getting insured. If you have a favorable credit score, insurance companies will offer you better premium rates on your car or life insurance, for example.

Potential employers may also look at your credit history during background checks. A good credit score will increase your chances of getting hired.

About Scoring System in the Philippines

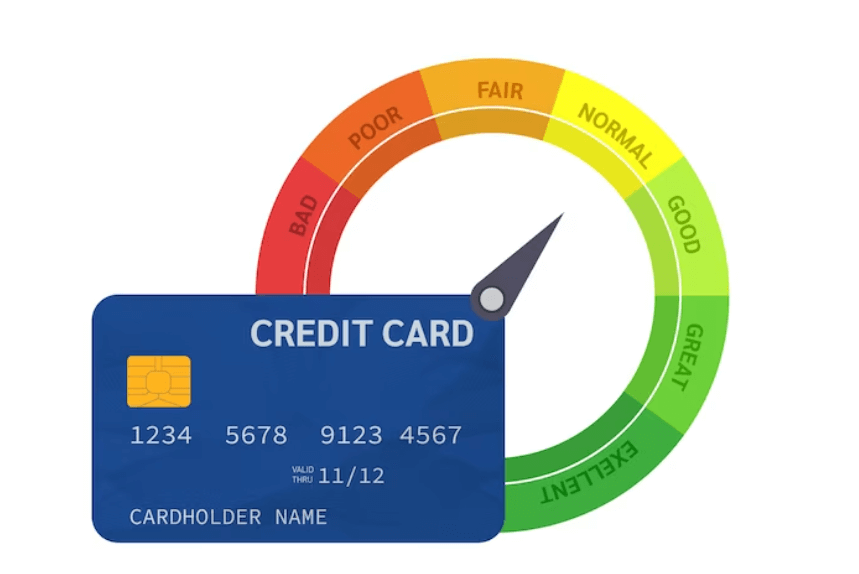

The credit score system in the Philippines ranges from 300 to 850, with 850 being the highest score you can possibly attain. If your score is around 800 to 850, it means that your credit standing is exemplary.

If you have a score ranging from 700 to 799, you have a good credit standing. A number between 650 to 699 is a fair score; a number between 600 to 649 is a poor score.

Anything below 600 means a bad credit score. If your score is 600 and below, you will have a hard time getting approved for loans, applying for credit cards, and even getting insurance policies.

To maintain healthy credit, try to keep your credit score at 650 and above.

What is a Good Credit Score in the Philippines?

There is no single number that can represent a good credit score in Philippines. Some lending services use numbers higher than 3,000, some higher than 600, and some use letters. To know what a good credit history is, you have to contact the reporting bureau of your choice. Generally speaking, an excellent credit score is above 750.

Need money that you can get quickly? Get fast loan online with Digido in just 4 minutes! The first loan for new clients is interest-free. Calculate your pre-approved loan amount:

* Interest payments are approximate. The final loan amount and interest rate must be confirmed in your loan agreement after loan approval.

10 Tips on How to Clear bad Credit history in the Philippines

Clearing or improving a bad credit history in the Philippines involves a series of steps, similar to those in many other countries. Here are some steps you can take to address a bad credit history:

- Obtain Your Credit Report: Before addressing your credit issues, you first need to know what they are. Obtain a copy of your credit report from the CIC or other credit reporting agencies recognized by it.

- Review for Inaccuracies: Make sure all the information in your credit report is accurate. If there are errors or discrepancies, you can dispute them with the credit bureau.

- Pay Outstanding Debts: Prioritize paying off your outstanding debts. If you can’t pay the entire amount at once, negotiate with your creditors for a payment plan or a reduced settlement amount.

- Negotiate with Creditors: If you have any negative items on your report, try negotiating with the creditor. Some might agree to remove or adjust the negative entry once you settle your debt or meet specific conditions.

- Maintain Good Financial Habits:

– Always Pay On Time: This is the most straightforward way to improve your creditworthiness over time.

– Limit New Credit Applications: Every time you apply for credit, an inquiry is made. Too many inquiries can negatively impact your credit score.

– Reduce Your Debt: Aim to keep your credit utilization low. The ratio of your debt to your available credit can significantly impact your credit score.

– Diversify Your Credit Types: A mix of credit (e.g., credit cards, personal loans, mortgage) can show lenders that you can manage different types of credit.

- Secured Credit Cards: If you’re having trouble obtaining a regular credit card due to your history, consider applying for a secured credit card. This type of card requires a cash collateral deposit that becomes the credit line for that account. By using it responsibly and paying off the balance on time, you can slowly rebuild your credit.

- Avoid New Negative Records: Ensure you don’t incur any new debts, late payments, or any other negative records as you’re trying to clean up your history.

- Regularly Check Your Credit: Keep an eye on your credit reports regularly to ensure that all information is accurate and that you’re making progress in improving your credit.

- Consider Credit Counseling: If you’re overwhelmed with managing your debts, you might want to seek the advice of a credit counselor or a financial adviser who can guide you on managing your debts and improving your credit score.

- Understand the Limitations: Negative information doesn’t stay on your credit report indefinitely. In the Philippines, as per the Credit Information System Act (CISA)[5], negative information will typically remain on your credit report for a maximum of seven years.

👉 Find out How to Take

a Fast loan Approval in 1 hour in the Philippines

a Fast Loans in 15 Minutes

How to Improve Your Credit Score in the Philippines

Once you have received your credit information and found out you got a low grade, the next step is to make sure that you make an effort to improve your credit score in the Philippines.

Here are some tips:

- Always pay your bills on time – institutions report to credit bureaus whether you are paying your utilities on time or not. This includes electricity, gas, water, phone bills, internet bills, credit card bills, and more.

- Keep debts low – do not borrow money so often and in large amounts.. But if you do, make sure you pay them on time. If you are not paying the full amount due, make sure that the amount you owe is small.

- Do not borrow money or apply for credit cards very often – Doing so will give the impression that you are heavily reliant on credit. Do not apply for different types of loans or credit at once. Before you apply for a new credit, make sure that you really need it.

- Do not close unused credit cards – if you have credit cards that you are not using, keep them open, but make sure you pay your annual fees and that they do not cost you a lot of money to maintain.

It takes a while to build a good credit score in the Philippines. The trick here is that you maintain a habit of being finance responsible. Do not take money that you cannot pay. If you get a loan or if you get approved for a loan or credit cards make sure you pay what you owe before the due date.

Loans with a Bad Credit Score in Digido

Just because you have a bad score does not mean you cannot get money. You can still get approved, especially in facilities like Digido.

The good thing about Digido Financial Corporation (with SEC Registration No.: 202003056) is that it is an honest company. It does not exploit a borrower with bad credit information by inflating the interest. Everyone is treated fairly here.

Here are the simple requirements to get money through Digido:

- You must be a Filipino citizen

- 21 – 70 years old

- 1 issued government ID

- Working mobile phone

As you can see, the requirements are really minimal. The best part is that Digido applications have so many benefits compared to traditional lenders or banks.

Here are the features of Digido:

- 0% interest for your first loan

You will not pay a higher interest rate just because your score in the Philippines is low.

- Easy Online Application (Web, mobile Apps)

You do not have to visit a physical location to apply for a loan. Everything is online. You will fill out the form online and also upload your documents.

- Fast Approval and Receiving Money within 5 minutes

Loans in Digido work in as short as 30 minutes; no need to wait for several days to be approved. The credit limit for the first free interest loan will be up to 3,000 pesos for 7 days and 25,000 pesos for future loans.

Apply nowWhether you have a high or low credit score or or you are blacklisted from Philippine banks, you can rely on Digido. All you get here is convenience, and you will not be exploited like you would if you applied for a loan from other conventional financial corporations. However, you still have to pay your bills on time. Otherwise, the facility will also rate you with a low score, and you will not be able to borrow next time.

If you have a Digido unpaid loan, you can extend it or contact the company on (02) 8876-84-84 and they will offer you a solution depending on your situation. Immediately after repayment you can apply for a new credit. Your payment should be made on time, and then the limit will increase. You can also make early repayment of an existing loan.

👉 Read about

OFW Loan one Day Process in the Philippines

a Cash Loans for Blacklisted in the Philippines

FAQ

-

How much does a credit report affect your score?In general, credit inquiries have a small impact on your Scores. For most people, one additional credit inquiry will take less than five points off their Scores.

-

How long does bad credit last Philippines?Most negative financial transactions will stay on your credit history report for about seven years

-

Can I go to jail for credit card debt in the Philippines?Filipinos with outstanding credit card debt will not go to jail because unpaid debts are only considered a civil, not a criminal offense.

-

How to clear bad credit history in the Philippines?To clear a bad credit history in the Philippines, obtain and review your credit report from the Credit Information Corporation (CIC) for inaccuracies. Pay off outstanding debts, negotiate with creditors, and maintain good financial habits such as timely payments and low credit utilization. Over time, good financial behavior will improve your credit history.

-

What is the Credit Score Calculator Philippines?The Credit Score Calculator is a part of TransUnion Credit Report, Score & Alert Services. It allows users to see how their current credit score might change based on future actions and events. The calculator is designed to help individuals understand the potential impact of various financial decisions on their credit score.

Authors

Digido Reviews

-

RonalynTheir service is superb! Thanks for the fastest and reliable service😍 Amazing app! Highly recommended! Thats all I can say🤩🤩🤩5

RonalynTheir service is superb! Thanks for the fastest and reliable service😍 Amazing app! Highly recommended! Thats all I can say🤩🤩🤩5 -

AnthonyNever thought it'd be this easy! Was searching for ways on how to clear bad credit history in CIC of Philippines, and then I stumbled upon Digido. Instant approval, even with my past credit issues! 👍5

-

ChristopherThank you for making me a valued customer. You gave me what I needed in times of desperate need for help. 5 stars for you Digido!5

-

WarrenFast disbursement and reasonable amount of interest. Thank you Digido4

-

JudithI was hesitant to apply because of what I saw on my credit report from Philippines. Thankfully, Digido didn't judge and helped me out when I needed it most! 🙏5

-

LloydFast and reliable. Firt time user here and was pleased how fast they provide you assistance. After I got verified it took only a minute and I got my cash.4

-

JaneHonestly, I was skeptical and stressed thinking about credit score in the Philippines, but thanks to Digido, I got approved quickly! I've been rejected by so many banks Digido surprised me!5

-

JeffreyI had diffuculty at first since I register my smart number but I wanted the disbursement in my Gcash globe number. I was advised to re enter it. I did it and voala, it was transfered and I was so touched that they lend me money with zero interest!!!! It's only 7 days but nowadays, nobody will give you cash without something in return for them. Job well done, Digido!4

Download our app

- Borrowing 24/7

- Approval rate over 90%

- 1 Valid ID