Debt Consolidation Loan the Philippines: Debt Settlement with a Single Loan

Key takeaways:

- With a debt consolidation loan, you can merge multiple debts into one single payment

- If you’re struggling with high interest rates, taking out a debt consolidation loan could be wise

- Digido provides a reliable and trustworthy lending option for Filipinos in need of financial assistance

Table of Contents

Do you find it challenging to manage numerous debts and make monthly payments on time? A debt consolidation loan in the Philippines may be the answer you need to streamline your finances and regain control. A single loan can streamline your payments and possibly cut your interest rates. Keep reading as we explore how a debt consolidation loan can financially help you get back on track!

What is Debt Consolidation?

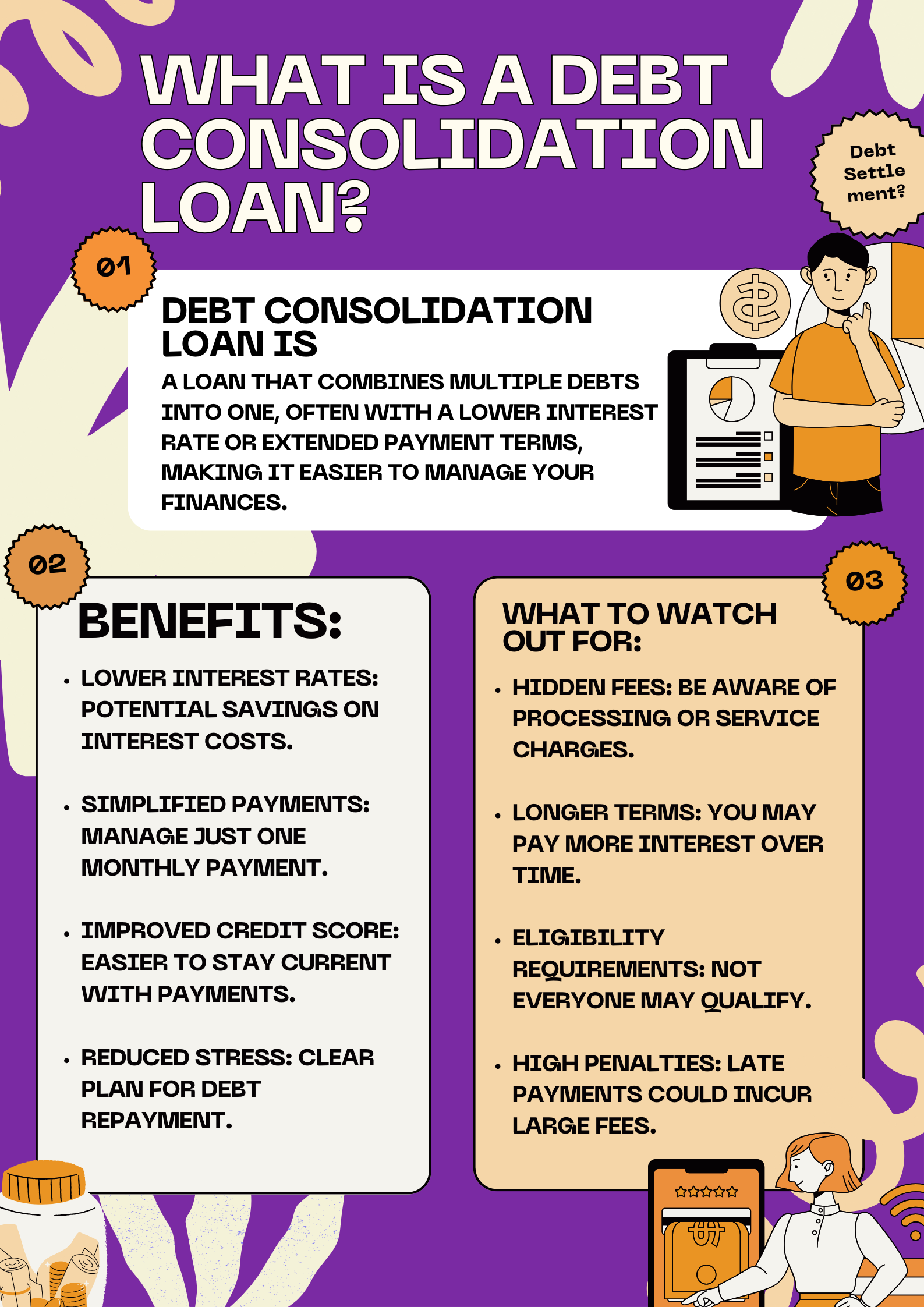

A debt consolidation loan allows a borrower to consolidate or combine numerous debts into a single loan. The funds from this loan can be utilized to settle outstanding balances on credit cards, personal loans, and other debts with high-interest rates, which can help borrowers manage their debt more effectively.

This can be done in two main ways: by taking out a debt consolidation loan or by transferring existing credit card debts to another credit card with better terms, known as a balance transfer. Both methods aim to reduce the complexity of managing multiple payments and may help secure lower interest rates.

- Only 1 valid ID needed to apply

- First loan with 0% interest rate

- Fast approval in 5 minutes

How Debt Consolidation Loans Work

Debt consolidation involves combining multiple debts into a single loan. This process allows a borrower to streamline their debt payments by consolidating their various debts into one account. The borrower receives a consolidated loan and makes a single monthly payment at a fixed amount, which is allocated towards repaying all the combined debts over a specified term. It simplifies how you pay back what you owe by having just one bill to worry about.

So, If you have several loans or credit card debts, a debt consolidation loan allows you to merge them into a single loan. Instead of managing multiple payments with varying interest rates and due dates, you only make one monthly payment.

5 Features of Debt Consolidation Loans:

- Debt consolidation loans often come with lower interest rates. This can reduce your overall interest costs and help you pay off the debt faster.

- Most consolidation loans have fixed terms, meaning you’ll pay a set amount each month, which helps with budgeting.

- You can choose from secured loans (backed by assets like your home) or unsecured loans (which don’t require collateral but may have higher interest rates depending on your credit score).

- The interest rate you get depends on your creditworthiness, financial stability, and risk level as evaluated by lenders. If your financial profile is strong, you may qualify for a lower rate.

- By consolidating, you make your debt more manageable and reduce the chance of missing payments, which could improve your credit score over time.

How Lenders Set Your Interest Rate When You Consolidate Debt

When you consolidate your debts, lenders use something called risk-based pricing to decide your interest rate. This means they look at how risky it is to lend you money based on factors like your credit score, how stable your income is, and any existing debts you have. If you have a more stable financial situation, you’re likely to get a lower interest rate.

By consolidating your debts at a lower rate, you not only simplify your payments but might also improve your credit profile. This could lead to better loan terms in the future, saving you even more money. Plus, with lower payments and quicker debt payoff, lenders may view you as a more reliable borrower.

Current Debt Trends in the Philippines

Consumer Credit in Philippines increased to 744.70 PHP Billion in the first quarter of 2024 from 722.46 PHP Billion in the fourth quarter of 2023. Consumer Credit in Philippines is expected to be 765.80 PHP Billion by the end of this quarter, according to Trading Economics global macro models and analysts expectations.

Currently, nearly half of the Filipino population carries some form of loan. These debts come in a variety of types, such as credit card balances, personal and microloans, as well as housing and auto loans, reflecting the widespread reliance on credit across the country.

The concerning news is that over ₱400 billion of these loans are classified as non-performing (or “bad loans”), meaning they are significantly overdue and unlikely to be fully repaid. This large volume of unpaid debt emphasizes the importance of debt consolidation as a critical measure for many Filipinos facing financial difficulty.

Benefits of Debt Consolidation Loan in the Philippines

Debt consolidation loans in the Philippines can help individuals merge multiple debts into a single loan with a lower interest rate and monthly payment, which can make it easier to manage finances and reduce debt. By consolidating debt, individuals can also simplify their financial obligations and avoid missing payments, which can negatively impact credit scores. When is debt Settlement in the Philippines a good idea:

👉 Deal with High-Interest Rates

Let’s say you are a borrower with a credit card with a 20% interest rate and a personal loan with a 15% interest rate. Consolidating such debts into a single loan with a 10% interest rate could save the borrower money.

👉 Organize Your Debts

Managing debts with different interest rates and due dates can be confusing and overwhelming. Consolidation of debts can simplify the process by combining all debts into a monthly payment. That can make it simpler for borrowers to manage their finances and ensure they don’t miss any payments.

Suppose you’re a borrower with multiple credit cards with different due dates. You can consolidate such debts into a single loan and make single monthly payments.

👉 Clear Your Debts Quickly

Debt consolidation loans can provide shorter repayment terms, helping borrowers settle their debts faster. For instance, suppose you have a credit card with a high balance. Having a high-interest rate will allow you to consolidate your debt into a new loan with a shorter repayment term. In turn, that will enable you to settle the debt sooner and save some on interest charges.

👉 Simplified Your Payments

Instead of juggling multiple payments to different creditors each month, a debt consolidation loan consolidates these into a single monthly payment. This simplification helps in better managing your budget and reduces the chances of missing payments.

👉 Improved Your Credit Score

By consolidating debt and making regular, timely payments, you can gradually improve your credit score. Consistently reducing your overall debt balance without accruing new debt is viewed positively by credit bureaus.

👉 Stop Increasing Debt

A consolidation loan can act as a stopgap to prevent further accrual of debt, especially from credit cards. By converting revolving credit into a term loan, you avoid the temptation to keep increasing credit card debt.

Is Debt Consolidation Right for You?

Debt consolidation might be your next smart move—if you answered “yes” to two or more of these key questions:

- Do You Have Multiple High-Interest Debts?

If most of your debts come with high-interest rates, consolidating them into one loan with a lower interest rate can save you money in the long run.

Take a detailed look at each of your debts—what are the interest rates, payment terms, and outstanding balances? Target those high-interest debts that are eating away at your finances. Those are the ones you’ll want to tackle first through consolidation, helping you regain control.

- Do you find it hard to manage different payments?

If keeping track of various due dates and payments feels overwhelming, simplifying everything into one monthly payment could ease your stress.

- Is your credit score better now than when you first took on your debts?

With an improved credit score, you might be able to get a consolidation loan with better terms than your existing debts.

- Are you committed to avoiding new debt?

Ask yourself: are you ready to commit to consistent payments? Debt consolidation can help reduce financial stress, but it works best if you’re committed to not accumulating new debt while paying off the consolidated loan. Think of it as a financial reset button that requires you to stick to the plan.

If you answered “yes” to two or more, debt consolidation might just be the right solution for simplifying your finances and lowering costs!

What Are the Types of Debt Consolidation

Debt consolidation loans are a popular option for people in the Philippines who are struggling with multiple debts. These loans allow you to combine all of your debts into one manageable loan with a lower interest rate and a longer repayment term. Here are the types of debt consolidation loans available in the Philippines:

✅ Personal Loan

This is a loan that you can take out from a bank or a financial institution. You can use the loan amount to pay off your existing debts and then make one monthly payment on the personal loan. These loans typically have fixed interest rates and terms, which can simplify monthly payments and potentially reduce the total interest paid.

✅ Balance Transfer Credit Card

Some credit cards offer balance transfer options, allowing you to transfer the balances from your high-interest credit cards to a new credit card with a lower interest rate. Balance transfer credit cards typically offer promotional interest rates for a limited time, usually 6 to 12 months.

For individuals with good credit, a balance transfer credit card that offers a 0% introductory interest rate could be a useful alternative. You can transfer your high-interest credit card debts onto this card and pay them off during the promotional period, typically between 12 to 18 months, without accruing interest. Be cautious, though—if you don’t pay off the balance during this period, the interest rate can jump significantly.

Several banks and credit card providers in the Philippines offer balance transfer credit cards, including:

- BDO Unibank

- Metrobank

- BPI

- Citibank

- HSBC

- Security Bank

- EastWest Bank

- RCBC

Each provider may have different terms and conditions for their balance transfer credit cards, such as the interest rates, fees, and promotional periods.

✅ Home Equity Loan

If you own property, you can take out a home equity loan. It allows you to borrow against the equity of your home to pay off multiple debts. This typically offers a lower interest rate compared to unsecured loans, but it does put your home at risk if you fail to make payments.

✅ Debt Management Plans (DMP)

A DMP may be a good option if the following apply to you: you can afford your living costs and have a way to deal with any priority debts, but you’re struggling to keep up with your credit cards and loans. you’d like someone to deal with your creditors for you. Making one set monthly payment will help you to budget.

✅ Government Debt Consolidation Programs

The Philippine government offers debt consolidation programs for people who have multiple debts with different lenders. The program allows you to consolidate your debts into one loan with a lower interest rate and a longer repayment term.

You can also try the option of informal negotiations: This involves directly negotiating with creditors to consolidate and restructure your debts. This may not be a formal program like other options, but it can result in lower interest rates or more manageable payment term.

Read more:

✦ All about our Credit Score

✦ Quick Loan For Unemployed: Is it Possible?

Where to Apply for Debt Сonsolidation in the Philippines

In 2025, debt consolidation in the Philippines can be applied for through various financial institutions, including banks, credit unions, and online lending platforms. Here are some popular options where you can apply:

Government Institutions

Here are some popular government debt consolidation programs in the Philippines:

- Pag-IBIG Fund Loan Consolidation Program (1) – offered by the Home Development Mutual Fund (Pag-IBIG), this program is available for members who have existing loans from the fund and other lenders. It allows you to consolidate all your loans into one with a lower interest rate and a longer repayment term.

- SSS Loan Conso Loan (2) – provided by the Social Security System (SSS), this program is available for members who have unpaid loans with the SSS. It allows you to restructure your loans and pay them off through a new loan with a lower interest rate and longer repayment term. Members may submit their application for the Conso Loan program online through their My.SSS account.

- GSIS Financial Assistance Loan (3) (GFAL). Program – offered by the Government Service Insurance System (GSIS), this program is available for members who have outstanding loans with lending institutions. It allows you to consolidate your loans into one with a lower interest rate and a longer repayment term.

- Credit Management Association of the Philippines (4) (CMAP) – While not a direct lender, CMAP can assist in negotiating with creditors to consolidate and restructure debts under terms that are manageable for the borrower.

Commercial Banks

Many private financial institutions offer debt consolidation services. These might not be government-backed but can offer competitive rates and are worth considering.

- BDO Unibank offers personal loans with flexible terms that can help consolidate debts.

- Bank of the Philippine Islands (BPI) provides personal loans specifically aimed at debt consolidation with competitive interest rates.

- Metrobank offers personal loans that you can use to combine multiple debts into one, simplifying payments.

Note: The information about loan providers presented in the text is subject to change and borrowers are advised to contact their chosen institution directly for the most updated information.

Credit Unions and Cooperatives

Cooperatives and credit unions are community-based lenders that often offer lower interest rates for consolidation loans. For example: Cebu People’s Multi-Purpose Cooperative (CPMPC) and other local cooperatives provide loans that members can use for debt consolidation at affordable rates.

Need money you can borrow quickly? Get up to PHP 25,000 in just 4 minutes! Calculate your loan cost and click ‘Apply Now’:

* Interest payments are approximate. The final loan amount and interest rate must be confirmed in your loan agreement after loan approval.

Requirements to Qualify for a Debt Consolidation Loan

Debt consolidation loans often have specific requirements that borrowers should meet to be qualified. Some of the requirements for this loan include the following:

- A Filipino citizen from 21 to 65 years old

- A minimum monthly income (some lenders require from Php 20,000 or more)

- Valid ID

- Collateral (for secured loans)

To be eligible for a debt consolidation Philippines, most providers require applicants to have a good credit report, payment history, and a stable income to ensure they can repay the loan. Essentially, they prefer applicants without red flags, indicating a high default risk. Some providers may also require collateral for more substantial loan amounts, such as a house or car.

If you have an imperfect credit report due to unpaid loans or credit card bills and need to consolidate your debts, you may want to explore other options with more flexible approval criteria.

Debt Сonsolidation Process

Here is a step-by-step guide to the debt consolidation process in the Philippines:

1. Assess Your Debt

Determine the total amount of debt you owe, the interest rates and fees you are paying, and the monthly payments you are making. This will help you determine if debt consolidation is the right option for you.

2. Choose a Provider

Research and compare the different debt consolidation options available in the Philippines, such as personal loans, balance transfer credit cards, and government programs. Consider the interest rates, fees, and repayment terms of each option.

3. Check Eligibility

Ensure you meet the provider criteria:

- Filipino citizen or resident.

- At least 21 years old but not older than 70 at loan maturity.

- With a stable income (employed or self-employed).

- Good credit history.

4. Apply for the Loan

Once you have chosen a provider, apply for the loan or credit card. Visit the provider’s branch or apply online through the official website. You will need to provide documentation such as identification, proof of income, and a list of your existing debts. Gather the necessary paperwork, including:

- A completed loan application form.

- Valid government-issued ID (e.g., passport, driver’s license).

- Proof of income (latest payslips, employment certificate, or financial statements if self-employed).

- Proof of existing debts (credit card statements, personal loan documents).

4. Wait for Approval

The lender will assess your application, including your credit score and income stability. Approval may take a few hours to days, depending on the complexity of your case. Once approved, the bank will disburse the funds to consolidate your existing debts.

6. Pay Off Your Debts

If approved, use the loan or credit card to pay off your existing debts. Make sure to follow the terms and conditions of the loan or credit card, such as making on-time payments. Keep track of your payments and make sure to pay on time to avoid additional fees and interest charges. It’s important to stick to your budget and avoid taking on additional debt while you are paying off your consolidated loan.

Risks of Debt Consolidation loan

Despite the fact that debt consolidation loans have a number of advantages described above, there are some pitfalls, which it is better to know about in advance. These points further highlight situations where consolidation of debts in the Philippines might not be beneficial:

- Misconceptions about Debt Elimination: If you believe that consolidating your debts will magically erase them, this can be misleading. Consolidation simply combines multiple debts into one payment; it doesn’t reduce the total amount owed.

- High Fees and Costs: Fees associated with debt consolidation, such as balance transfer fees, annual fees, and possibly high interest rates, can add up. If the fees or the new loan’s interest rate are too high, the financial benefits of consolidation could be negated.

- Extended Payment Terms: By extending the term of the loan to lower monthly payments, you might end up paying more in total interest over the life of the loan. This could make the overall debt more expensive than the original debts.

- Risk of Missing Payments: If you’re prone to missing payments, consolidating your debts into a single larger loan could increase the risk of significant penalties and fees, exacerbating your financial situation.

- Small and Manageable Debts: For smaller debts that can be paid off relatively quickly, consolidation might not be necessary and could even be more costly when considering fees and potential interest rate changes.

| Pros | Cons |

|---|---|

| ✓ Interest rates are lower ✓ Monthly payments are reduced ✓ Simplified debt management ✓ Improved credit score |

✕ Possible increase in the total amount paid ✕ Default and foreclosure risks ✕ Potential for higher long-term costs ✕ Payment of hidden fees or penalties |

Alternatives to Debt Consolidation Loan

If you’re considering debt consolidation but aren’t sure if it’s the right fit for you, there are several other options to explore that may better suit your financial situation. Here are some alternatives:

Debt Snowball or Avalanche Method: These are self-managed strategies for paying off debt. The debt snowball method focuses on paying off your smallest debt first, then moving on to the next smallest, building momentum as you go. The debt avalanche method targets debts with the highest interest rates first, minimizing the overall interest paid over time. Both methods provide structure to debt repayment without the need for new loans.

Debt Management Plan (DMP): If managing your debts on your own seems overwhelming, a debt management plan offered by credit counseling agencies might be a good option. A DMP consolidates your debts into one payment, but it differs from a loan because your credit counselor negotiates lower interest rates or fees with your creditors. You’ll make one monthly payment to the counseling agency, which distributes it to your creditors.

Debt Counseling: Credit counselors work with you to evaluate your financial situation and develop a plan tailored to your needs. They can help you understand your debts, spending habits, and ways to improve your financial management. One of the main services offered by credit counseling agencies is the creation of a Debt Management Plan. Through a DMP, your credit counselor negotiates with your creditors to lower interest rates, eliminate late fees, and reduce your monthly payments. You make one payment to the counseling agency, which then distributes it to your creditors.

Debt Settlement: Debt settlement involves negotiating with your creditors to pay a lump sum that is less than the total amount you owe. This can be a risky option, as it can negatively impact your credit score, and there’s no guarantee your creditors will agree. It’s typically used when you’re already struggling to make payments and are at risk of default.

Bankruptcy: Filing for bankruptcy should be considered a last resort, but it is an option for those who are deeply in debt and unable to meet their financial obligations. Bankruptcy can either discharge most of your debts (Chapter 7) or create a repayment plan (Chapter 13). However, it has long-term effects on your credit score and ability to borrow in the future.

7 Tips on How to Manage Debt on Your Own

- Know how much you owe.

Gather all your financial statements, credit card bills, and loan documents to determine your total debt. - Admit that you need help.

Seek advice from a financial advisor or a credit counselor to help you manage your debt. - Set up a payment calendar.

Create a schedule to monitor your payments and dodge late fees or missed payments. - Decide which debt to pay off first.

Prioritize debts with high-interest rates or those with the smallest balance. - Prioritize debt payments.

Allocate more money to pay off debts with high-interest rates or those that are overdue. - Reduce expenses.

Cut down on unnecessary expenses, avoid impulse buying, and create a realistic budget to manage your finances. - Increase income.

Consider taking on a part-time job, selling unused items, or negotiating a salary increase to boost your income and pay off your debt faster.

Read more: How to Apply for

✦ Fast Loan in 15 Minutes

✦ Loan with Minimum Documents

Why people choose Digido for Personal Loans

Digido provides a convenient and efficient way to finance with a range of loans, from 0% interest for first-time borrowers to unsecured loans of up to PHP 25,000 for repeat borrowers. Digido offers a fast and flexible application process, competitive interest rates, no collateral requirements and the ability to use the remaining funds for any purpose.

There are several benefits to using Digido for your personal loan needs, including:

- 0% interest for first loan

- Easy online application process

- Only 1 valid ID needed to apply

- Quick loan approval in 5 minutes

- Use of funds for any purpose

- No collateral is required

- No proof of income is required

Digido offers a convenient and accessible way to get a personal loan in the Philippines. Their easy application process, quick loan approval, and flexible loan amounts make it a great option for those who need funds quickly and without hassle.

Apply now

Summary

To sum up, a debt consolidation in the Philippines can simplify your finances and possibly diminish your interest rates by combining multiple debts into a single loan.

These loans can offer shorter repayment terms to help you pay off your debts faster. However, consider the potential risks and disadvantages of debt consolidation loans, such as a possible increase in the total amount paid and the impact on their credit score.

Learn more: How to Get

✦ Personal Online Loan up to PHP 25,000

✦ Fast Emergency Loan online

FAQ

-

Does debt consolidation worsen your credit rating?Debt consolidation can worsen your credit score in the short term due to the credit inquiry and new account opening. Still, it can also improve your score in the long run by reducing your debt-to-credit ratio and improving your payment history

-

Can I still apply for a debt consolidation loan if I have a bad credit score in the Philippines?Yes, you may still apply for a debt consolidation loan in the Philippines even if you have a bad credit score, but the chances of approval may be lower, and the interest rates may be higher.

-

What happens if I miss a payment on my debt consolidation loan in the Philippines?If you miss a payment on your debt consolidation loan in the Philippines, it can negatively impact your credit score, and you may incur late fees or penalties. It's important to contact your lender as soon as possible to discuss your options.

-

How long does it take to pay off a debt consolidation loan in the Philippines?The length of time it takes to pay off a debt consolidation loan in the Philippines depends on various factors, such as the loan amount, interest rate, and payment terms. Typically, it can take several years to pay off a debt consolidation loan, but this can vary depending on individual circumstances.

-

Why is Debt consolidation as a short-term fix?A debt settlement loan can be a short-term fix because it does not address the root cause of debt: overspending and living beyond one’s means. Pairing debt consolidation with a budget and lifestyle change is essential to ensure long-term financial stability.

Authors

Download our app

- Borrowing 24/7

- Approval rate over 90%

- 1 Valid ID