Title Loans in the Philippines: Your Complete Guide to Asset-Based Borrowing

Table of Contents

Wait, you need quick cash to spend on something important? Well, there’s a way to obtain funds quickly without surrendering much at first with title loans. If you have a car, or maybe a land property, you can easily get money by giving the lending agencies your asset or property title.

But as much as this is a quick and easy way of getting your hands on a few funds, there are risks involved. Through this article, you will learn the process, risks, and benefits of title loans and other options that you can use to obtain funds.

- Apply with only one valid ID

- Fast approval in 5 minutes

- First loan with 0% interest rate*

What is a Title Loan?

If you are not that familiar with title loans, let’s try to learn the basics about it first before we dive deeper into this guide.

To start with this guide, basically, a title loan is a method of secured borrowing arrangement where from your assets and properties, you can obtain quick funds for emergency use.

Now, there are many ways that these loans are known in the Philippines, and some of the more popular terms are “sangla” or “prenda.” These methods of obtaining funds have been popularized because of their accessibility and straightforward process. The bonus of using your assets is that you can qualify for larger amounts, as well as fewer credit checks. But wait, let’s break down how much of a bargain this is.

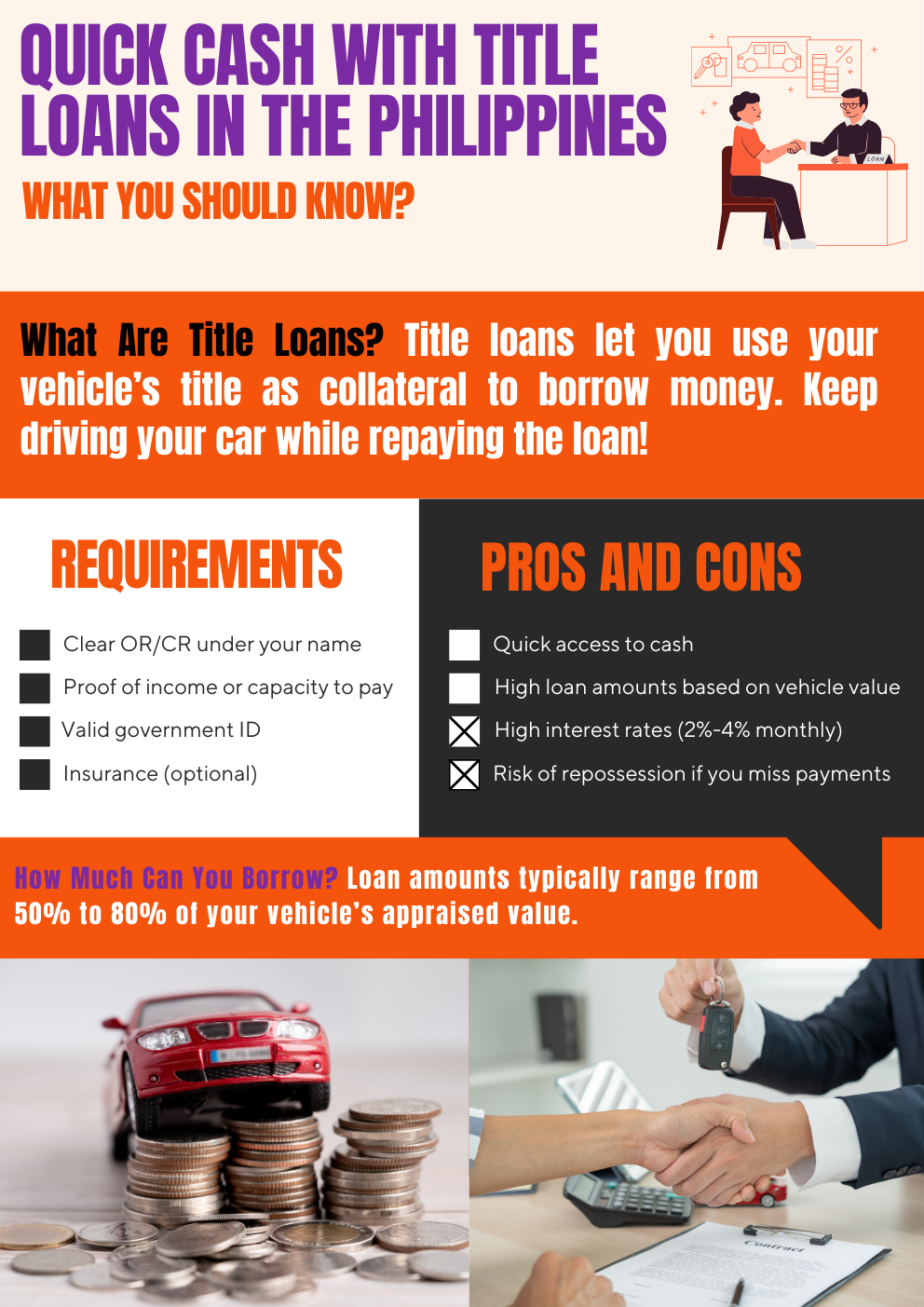

A Title Loan is a type of secured loan where the borrower uses their vehicle (car, motorcycle, or other vehicles) as collateral. The lender holds the vehicle’s title as security for the loan, and the borrower can continue to use their vehicle while repaying the loan.

However, there are many Filipinos that actually use this method of obtaining money not for emergency use, but just for quick cash, making this process a bit risky for some. Therefore, it is very important to understand all the features of such loans.

Key Features of Title Loans

- Collateral Requirement: The vehicle’s title must be lien-free or have minimal debt associated with it.

- Short-Term Loan: Title loans are typically short-term, with repayment periods ranging from 15 to 30 days.

- High Interest Rates: They often come with high-interest rates and fees, making them an expensive borrowing option.

- Quick Access to Funds: They are popular for their fast processing, often providing cash on the same day.

- Risk of Repossession: If the borrower fails to repay the loan, the lender has the right to repossess and sell the vehicle to recover their money.

How do Title Loans Work?

The moment that you exchange your assets or properties with the lending agency, you temporarily surrender the official title or deed while keeping physical possession of the asset. This process provides security to the lender while allowing you to continue benefiting from the property that you processed for a title loan, throughout the term of the loan.

What is the Cost of a Title Loan Based on?

It would seem that here is the asset, here are the guarantees against non-payment. So why can rates be high? While collateral does reduce some risk for lenders, it doesn’t eliminate the factors that justify high costs in their business model.

Title loans have high costs despite being secured by collateral due to several factors:

1. High Risk for Lenders

Default Risk: Borrowers who take title loans often have poor credit or limited financial stability, making them more likely to default. Even though the lender can repossess the vehicle, the resale value may not always cover the loan amount and associated costs.

Depreciating Asset: Vehicles lose value over time, and if the car’s worth drops significantly, the lender may incur losses.

2. Short Loan Term

Title loans are typically short-term (15–30 days), which means lenders need to charge higher fees and interest rates to make the loan profitable. A small principal amount combined with high fees over a short period results in a very high annual percentage rate (APR).

3. Lack of Credit Check

Title loans are often marketed as “no credit check” loans, which increases the lender’s risk. To offset this, they charge higher fees and interest rates.

4. Administrative Costs

Handling collateral (e.g., verifying and holding a vehicle title, repossessing and reselling vehicles in case of default) involves administrative costs that lenders pass on to the borrower.

What Types of Assets are Accepted for a Title Loans?

Title loans typically accept vehicles such as cars, motorcycles, trucks, or SUVs as collateral. Some lenders may also accept other valuable assets like boats or heavy equipment, depending on their policies.

Car Title Loans

When you apply for a car title loan, you pledge your vehicle’s ownership document (the OR/CR) as security. Lenders evaluate the car’s value, your capacity to pay, and the loan amount requested. Typically, the loanable amount ranges from 50% to 80% of the car’s appraised value.

Borrowers retain the use of their car during the loan period, but the lender holds onto the title. If the borrower fails to repay, the lender can repossess and sell the vehicle to recover the loan amount.

The most common type of auto title loans involve using the vehicle as collateral for the funds obtained. Some of the common vehicles used for collaterals are:

- Private cars and SUVs

- Motorcycles

- Commercial vehicles

- Trucks and heavy equipment

Pros of Car Title Loans

- Quick Approval: Most lenders process applications within 24-48 hours.

- High Loan Amounts: Loan amounts depend on the vehicle’s value, making it easier to access larger sums compared to unsecured loans.

- Flexible Usage: Funds can be used for emergencies, debt consolidation, or business needs.

Costs and Risks

- High Interest Rates: Interest rates on car title loans in the Philippines are typically higher than those on traditional secured loans. Monthly interest can range from 2% to 4%, leading to significant costs over time.

- Risk of Repossession: Failing to repay the loan on time could result in losing your vehicle.

- Additional Fees: Some lenders charge processing fees, appraisal fees, and penalty fees for late payments.

Requirements for Car Title Loans

To apply for a car title loan, you’ll generally need:

- A clear title (OR/CR) under your name.

- Proof of income or capacity to repay.

- Valid government-issued ID.

- Comprehensive insurance (sometimes required by lenders).

Getting Loans with

a Car as Collateral in the Philippines

Real Estate Title Loans

Aside from vehicles, property owners can also leverage the value of their homes and other real estate establishments to acquire funds. Some of the more popular real estate properties used are:

- Residential properties

- Commercial buildings

- Vacant lots

- Agricultural lands

Other Valuable Assets

If ran out of viable options, you may also consider other valuable assets like the following:

- Industrial equipment

- Construction machinery

- Precious metals and jewelry

- High-value collectibles

Terms and Conditions of Title Loans in the Philippines

The value and interest rates that you get will mainly depend on the assets that you set as collateral for title loans. Furthermore, the options for each asset will vary from different lending agencies. For a more general idea about the possible value and interest rate range, here’s a quick overview.

| Asset Type | Typical Loan Value | Interest Rate Range | Processing Time | Term Length |

|---|---|---|---|---|

| Auto Title Loans | 50-70% of value | 1-4% monthly | 1-3 days | 3-12 months |

| Real Estate Title Loans | 60-80% of value | 0.8-3% monthly | 5-10 days | 1-5 years |

| Equipment Title Loans | 40-60% of value | 2-5% monthly | 2-5 days | 6-24 months |

| Jewelry Title Loans | 30-50% of value | 2-4% monthly | Same day | 1-6 months |

Safety and Legal Protections

In the process of going through title loans, there are laws and policies that have been implemented by different governing bodies to protect lenders and borrowers. At the same time, these rules and guidelines create a fair and transparent environment that will not make the process intimidating for many.

- Republic Act No. 3765 (Truth in Lending Act) (1)

In understanding the contents of each contract, terms and conditions, and other agreements, RA 3765 was constituted to protect lenders and borrowers. This Republic Act generally ensures that the borrower is fully aware of the terms and conditions, which include interest rates, fees, and other charges. This process of transparency helps prevent borrowers from falling into debt from the loans processed.

- Bangko Sentral ng Pilipinas (BSP) Circular No. 1133 (2)

Bank agencies also help the process of lending by setting ceilings on interest rates and other fees charged by the lending and financing companies. For example, BSP Circular No. 1133 ensures that interest rates and fees are reasonable and not too excessive. This regulation implemented by the BSP prevents borrowers from being exploited by high-cost loans which can lead borrowers to debt if not enforced.

- Securities and Exchange Commission (SEC) Guidelines (3)

The Lending Company Regulation Act and other relevant laws and guidelines imposed by the SEC help protect borrowers from unfair practices. This also sets and ensures that lenders operate within the correct legal framework.

Together, these laws and regulations help provide a safer lending environment by promoting transparency and fair collection practices. It also protects borrowers from the right to prepay without excessive penalties.

Quick Cash Loans Without Collateral:

The Benefits of Unsecured Loans

Where to Get a Title loan in the Philippines?

In the Philippines, title loans are typically referred to as pawning loans or collateral-based loans and are offered by various financial institutions, including pawnshops, banks, and private lending companies. Here are some common options for obtaining a title loan in the Philippines:

✅ Some Banks offer secured loans using vehicles or real estate titles as collateral. Examples:

- BPI Family Savings Bank: Offers secured loans with flexible repayment terms.

- Security Bank: Provides secured loans for higher amounts using vehicles or properties.

Advantages: Lower interest rates, trusted institutions. However, you need a good credit history, and you need to gather a lot of documentation.

✅ Pawnshops like Cebuana Lhuillier or M Lhuillier accept vehicle titles or high-value items as collateral for loans.

Advantages: Easy to qualify for, quick processing. Require a clear title, government-issued ID, proof of ownership.

Learn all about

Cebuana Lhuillier in the Philippines

✅ Private Lending Companies. These lenders specialize in title loans, particularly for vehicles or real estate. Examples:

- Radiowealth Finance Company (RFC): Offers loans with vehicles as collateral.

- Asialink Finance Corporation: Specializes in auto-title loans.

Advantages: Flexible terms, quicker approval. Caution: Verify legitimacy and ensure they are registered with the SEC.

✅ Some Cooperatives provide loans to members using vehicle titles or land titles as collateral.

Advantages: Lower interest rates compared to private lenders. Don’t forget that you must have cooperative membership.

Title Loan Application Requirements and Process

1. Prepare Standard Documents

- Each lending agency will have its own requirements, but in general, at least one (1) Valid Government-issued ID is enough to start with your application process.

- Aside from that, you may also need to prepare the original property title or deed for the asset.

- It is also advised to prepare your proof of monthly income or capacity to pay.

2. Application Process

There are two methods to apply for a title loan. Other lending agencies will have a website where you can apply or you will have to visit the nearest branch. During the application process expect the following:

- Choosing the method of obtaining the funds.

- The process to repay the loan.

- Signing of contract with the lending agency.

3. Evaluation Process

After sending in your application and signing the contract, the lending agency will evaluate all details that you forwarded. Agencies will also take a look at your capacity to pay the loans and the other history in lending. If you have a great background in lending and have a good history with the agency, you will have a high chance of approval.

4. Receive the Funds

Once the lending agency evaluates your application, you will receive an email, text message, or a call from one of the representatives to confirm. After a few minutes, you will ideally receive the funds on the method and platform you chose to obtain the funds.

Risks and Benefits of a Title Loans

| Aspect | Benefits | Risks |

|---|---|---|

| Quick Access to Funds | Title loans can provide fast and easy access to cash, which can be helpful in emergencies and urgent situations. | High interest rates can make repaying a bit of a challenge. |

| Use of Assets as Collaterals | You can use your car, home, or other valuable assets as collateral, allowing you to borrow larger amounts. | If you default on the loan, you risk losing the asset you marked as collateral. |

| No Credit Check Required | Title loans oftentimes don’t require a credit check, making these loans more accessible to individuals with poor credit history. | The loan amount will highly depend on the value of your asset, which may not cover all your financial needs. |

| Maintain Asset Use | You can still continue to use your assets (e.g., driving your car or living at your home) while repaying the loan. | Failure to meet repayment deadlines can result in repossession of your asset. |

Housing Loans for Renovation:

The Optimal Home Improvement Loans

Tips on Risk Management and Smart Borrowing

When taking loans from lending agencies, it would typically involve several expenses. Some of the more common expenses come from

- Interest charges: Like banks, interest charges are the main source of revenue for lending agencies. They lend you money and charge interest on it to compensate for the risk they’re taking to lend you the money.

- Processing fees: These fees cover the administrative costs of processing the loan. This includes activities like evaluating your applications, verifying your information, and disbursing the funds.

- Insurance premiums: Some loans require insurance to protect the lender in case you default on the loan. The cost of this insurance is often passed on to you as a premium.

- Documentation costs: The lending agencies would take time and budget to prepare the necessary legal documents for the loan. Lenders charge documentation fees to cover these costs.

- Potential penalties: Penalties for late payments or early payments (prepayment penalties) are used to ensure borrowers stick to the agreed schedule. They also compensate the lender for the inconvenience or loss of anticipated interest.

Protecting Your Assets

When setting your assets as collaterals for title loans, always make sure that you take all the steps to secure and protect your assets. Here are some tips on how to:

- Maintain comprehensive insurance: By having your own comprehensive insurance process, you can protect your assets from damage or loss due to accidents, theft, or natural disasters.

- Keep detailed payment records: With your own record of payments, you can show proof of your timely payments and help track your loan repayment process. This will come in handy for any issues with the agencies losing track of your payments.

- Request regular statements of accounts: By requesting the statements of accounts from the lending agencies, you can check the payments made, interest accrued, and remaining balance.

Learn more:

The Ins and Outs of Home Equity Loans Philippines

Alternative Financing Solutions

Title loans are generally used by borrowers in need of quick cash for emergencies or short-term financial needs. However, due to their high costs and risks, financial experts often recommend exploring other options first.

| Options | Key Features | Best For | Consideration Factors |

|---|---|---|---|

| Bank Loans | Lower interest, longer terms | Stable income earners | Strict requirements |

| Pawnshops | Quick cash, simple process | Small, short-term needs | Higher interest rates |

| Credit Cards | Flexible credit line | Regular expenses | High APR |

| Microfinance | Group lending, smaller amounts | Small businesses | Regular payments |

| Digital Lending | Fast online process | Tech-savvy borrowers | Limited loan amounts |

Quick Digido loans for Your Emergency Needs

Digido is a legitimate and regulated lender in the Philippines, ensuring your borrowing experience is secure and aligned with industry standards.

Right now you can get a fast loan without interest for a first time borrower!

Why Choose Digido Over Title Loans?

- Lower Risk: You don’t risk losing a vehicle or asset as collateral.

- Online Application: You can apply for a loan entirely online, eliminating the need to visit a physical branch.

- Quick Approval: Many applications are approved within minutes, and funds are disbursed on the same day.

- Single Document Requirement: Digido makes it easy by requiring only one valid ID, such as a government-issued ID. There’s no need to submit numerous documents or undergo complex verification processes.

Need Quick Cash? Apply now with just 1 government valid ID. Calculate your pre-approved loan amount:

* Interest payments are approximate. The final loan amount and interest rate must be confirmed in your loan agreement after loan approval.

Conclusion

Title loans offer a quick way to obtain funds that are perfect for emergency situations. It offers viable financing solutions for Filipinos who own valuable assets and need access to funds. While it may provide flexible and quick cash, careful consideration of terms, costs, and risks is essential.

Frequently Asked Questions

-

What types of property can I use for a title loan?Most assets with value and with clear titles can be used for a title loan. This list includes vehicles, real estate, equipment, and precious metals.

-

How long does the entire process typically take?Processing time varies from the type of asset and the lender, ranging from same-day approval for small loans to a few days for larger values.

-

What happens if I struggle with repayment?Prolonged defaults or missing the schedule of repayment may result in property forfeiture. Contact your lender immediately to discuss options like restructuring. One good example of restructuring was during the pandemic when most banks restructured the repayment scheme for most borrowers.

-

Are there prepayment penalties?This varies by lender. Many allow early repayment with minimal or no penalties but always check the terms and conditions with the lender.

-

How is the loan amount determined?Lenders typically offer 40-80% of the asset’s appraised value, depending on the asset type, conditions, and market factors.

Articles sources

- 1. REPUBLIC ACT No. 3765 - AN ACT TO REQUIRE THE DISCLOSURE OF FINANCE CHARGES IN CONNECTION WITH EXTENSIONS OF CREDIT

- 2. BANGKO SENTRAL NG PILI PINAS - Ceiling/s on Interest Rates and Other Fees Charged by Lending Companies (LCs), Financing Companies (FCsl, and their Online Lending Platforms (OLPs)

- 3. SEC WEBSITE - About Lending Companies and Financing Companies

Authors

Download our app

- Borrowing 24/7

- Approval rate over 90%

- 1 Valid ID